Back

Copy

Share

Like

market

Polarization is proven by data.

Polarization is proven by data.

Polarization is proven by data.

A complete survey of 600 visitors at a major shopping mall found that both budget-friendly stores like Daiso and Olive Young and luxury boutiques are performing well at the same time. Polarization has been proven by the data. Card transaction data only shows the outcomes. The next battleground for next-generation retail consulting is telecom-based movement tracking and turning foreign consumer shopping routes into data.

A complete survey of 600 visitors at a major shopping mall found that both budget-friendly stores like Daiso and Olive Young and luxury boutiques are performing well at the same time. Polarization has been proven by the data. Card transaction data only shows the outcomes. The next battleground for next-generation retail consulting is telecom-based movement tracking and turning foreign consumer shopping routes into data.

A complete survey of 600 visitors at a major shopping mall found that both budget-friendly stores like Daiso and Olive Young and luxury boutiques are performing well at the same time. Polarization has been proven by the data. Card transaction data only shows the outcomes. The next battleground for next-generation retail consulting is telecom-based movement tracking and turning foreign consumer shopping routes into data.

Article Highlights

Not a crisis, but the disappearance of the 'middle ground': The retail market has entered a phase of extreme polarization rather than collapse, and consumers are practicing selective spending by opening their wallets only where value is clear at either extreme—Daiso’s cost-effective beauty products and high-priced luxury goods at department stores.

A data-proven 'malling' routine: A complete survey of 600 visitors to large shopping malls confirmed a clear movement pattern in which they 반드시 stop by Daiso and Olive Young at the beginning and end of their shopping trips, suggesting that purpose-driven visits to meet everyday needs have become the mainstream beyond simple shopping.

'Monetizing traffic flows' beyond the limits of card data: Going beyond traditional data that only shows payment outcomes, micro-analysis that precisely combines telecom-based real-time movement paths and foreign consumer spending patterns (e.g., PayPal) will become a core consulting capability that determines future asset value.

Official real estate market data points to shrinking supply and weakened consumption, but the on-the-ground sentiment in practice is different. It is the result of a mix of income structures of individual assets that are not captured in statistics, irregular consumer movement paths, and the distorted vacancy fatigue created by a traditional supplier-centric mindset. So, has the retail market truly reached its end? Or are new opportunities hidden where we have not looked? The current crisis is not a market collapse, but merely an advancement of business formats that demands a sophisticated, data-driven perspective. Through an interview with Deputy Manager Stella Jung of the CBRE Retail Consulting Team, we examine the real reason we must go beyond simple location theory and identify the micro-level competitiveness of individual assets.

Retail Consulting That Designs Purpose

Q. What is the consulting team’s practical role and position in the real estate development process?

Every real estate development begins with setting the purpose of a site before purchasing the land. The consulting team is the department that draws the initial blueprint at this very front stage, then intervenes in the process as constructors and developers join and revenue scale is estimated, laying the groundwork for disposition and leasing. In other words, consulting is the department that first encounters market information and forecasts what development scenarios will unfold ahead.

Q. There are many diagnoses that the retail market is in crisis lately—what is the actual atmosphere felt in the field?

People around us say commercial facilities have failed, but what we feel in the field seems completely different. Sales at major retail assets are currently soaring (including department stores and retail malls), and the “malling” phenomenon—where consumers solve everything from start to finish in one place—is becoming even more evident. In particular, because Korea is heavily affected by seasons and weather, there is a strong tendency to complete all routines inside one building without going outside, and this is proven by the overwhelming performance of large mixed-use shopping malls such as Starfield.

A quiet view inside a retail mall in the morning. After lunchtime, it becomes crowded even on weekdays with nearby residents and visitors.

It’s Not That People Aren’t Spending—It’s Just Polarized

Q. What interesting common pattern was found in the actual movement paths of large shopping mall visitors?

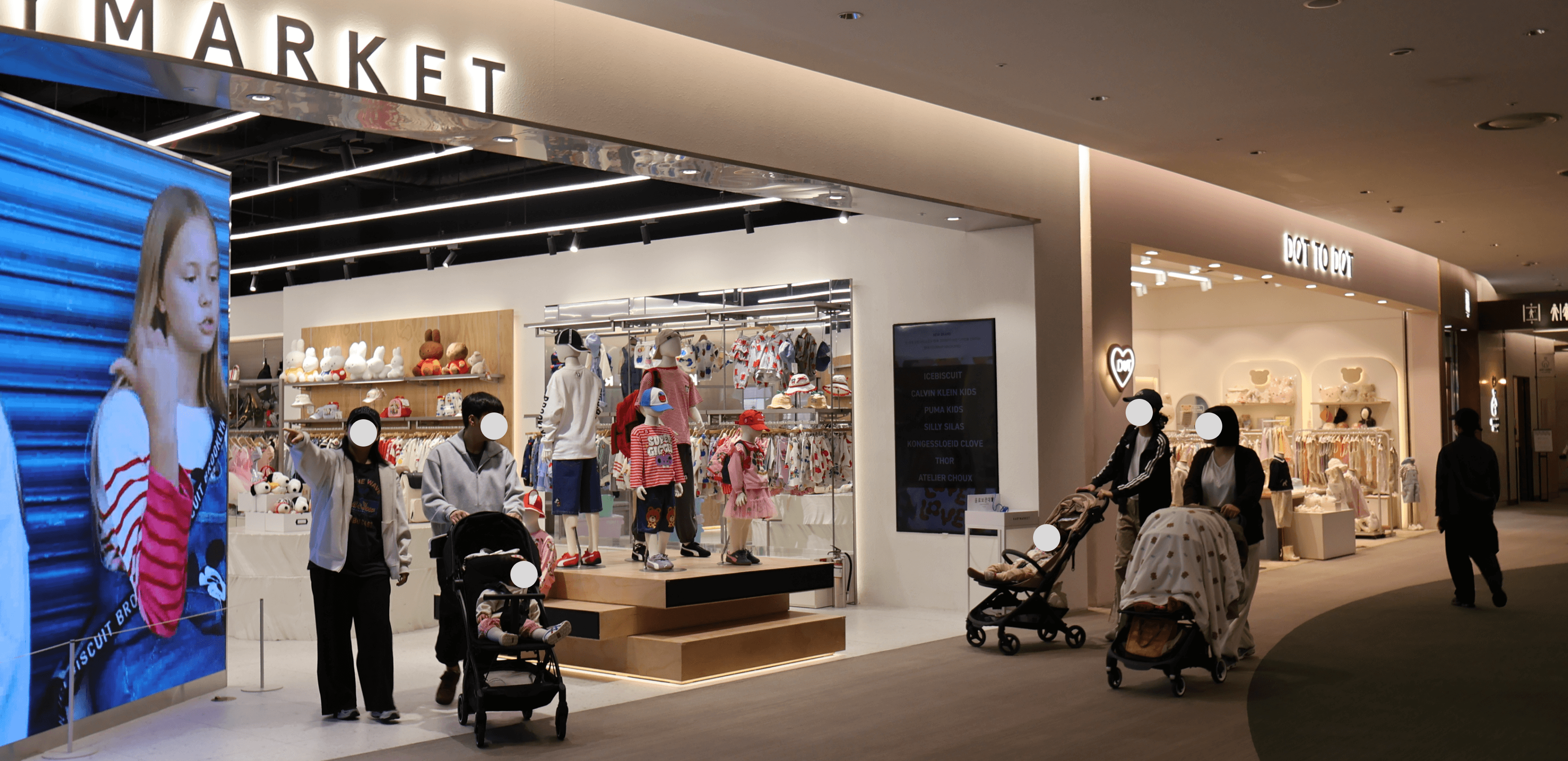

A recent three-month full-scale survey of 600 visitors at a major shopping mall drew a very clear consumer persona. A large share of visitors showed a routine of 반드시 stopping by Daiso and Olive Young when entering or leaving the mall, suggesting that consumers visit malls not only for glamorous shopping but also to satisfy practical daily needs. This also shows the tremendous influence of Daiso and Olive Young, but luxury stores are also performing well, and we can clearly confirm that polarization is deepening.

An Olive Young located inside Lotte World Mall.

Q. How significant is the status of Daiso and Olive Young within retail malls?

Retail trends that were previously encountered only through articles or rumors were fully proven with numerical data through this consumer behavior study. In particular, Daiso demonstrates strong customer-drawing power regardless of nationality in both residential trade areas and tourist districts such as Dongdaemun, serving as a core retail anchor.

The most notable point is Daiso’s cosmetics section. Its popularity is so high that foreign tourists buy products by the box as soon as they are stocked, meaning it now has very high potential to emerge as a strong competitor to Olive Young. A representative case is Zoom by Jung Saem Mool, a Daiso-exclusive line recently launched by JUNGSAEMMOOL Beauty. User reviews are pouring in saying this product line delivers overwhelming quality beyond simple price merit. Since items such as cushion foundations that used to cost in the KRW 40,000 range can be purchased at Daiso for around KRW 5,000, sold-out chaos occurs immediately upon release, to the point that it is hard even to browse products on the shelves.

Daiso cosmetics shelves are filled with a wide variety of cosmetic products.

Q. What pattern does consumer polarization observed in retail assets recently take?

The current retail market is in a state of severe polarization where the middle ground has disappeared. Even looking only at shopping malls, ambiguous luxury brands struggle, while high-end luxury performs above maintenance levels. Even after several price increases, consumers are boldly investing in luxury jewelry and high-priced bags while simultaneously buying low-priced daily necessities at Daiso and getting nail art—showing consumption behavior where they open their wallets intensively only in places that offer clear personal value.

Q. Why do you analyze that department store sales continue to rise beyond the inflation rate?

Because due to consumption polarization, the sales portion from VIP customers remains overwhelmingly dominant. In addition, select shops such as emerging designer brands and Musinsa premium lines have successfully taken hold and are absorbing trend-sensitive demand. Sales growth in the 6% range, exceeding inflation, is the result not merely of price hikes but of the advancement of these high value-added brands and premium food halls.

“Experience in the Mall, Payment on the Phone”: The Lowest-Price Wall Toy Stores Couldn’t Overcome

Q. In kids-targeted spaces, which category is underperforming in sales contrary to expectations?

Common sense suggests that kids cafés or large toy stores would have high sales, but actual data shows otherwise. Parents visit kids floors most frequently with their children and let them experience products, but actual purchases often happen online after searching for the lowest internet price on site, so it does not translate into offline sales. Those raising children may know this even better—the moment kids play with toys is often only that moment. After all, the place where you can hand a child ten thousand won and fill both hands with satisfaction is probably Daiso. Even if there is nearby residential demand, this is why sales at toy-selling facilities are lower than expected.

Q. Then what is the secret of brands that generate overwhelming sales on kids floors?

According to a recent field survey at a shopping mall, New Balance Kids ranked No. 1 in sales on the kids floor. This is because parents and children can share the brand, and functional trust has been secured through products like shoes designed for children’s comfort and activity. The retail winners are no longer spaces only for children, but value-sharing brands where parents’ taste and children’s practicality intersect. Parents and children can match outfits, and they can buy shoes in the same design.

A Generational Shift in Data

Q. What are the limitations of card sales data that has been widely used?

Card sales data has now become so public that even public institutions open it, so it is no longer a differentiated source. Card records only show the result of spending money, and cannot identify behaviors such as entering a store and doing only window shopping without purchasing, or movement paths. It is insufficient for explaining specific causality about where consumers came from and why they came.

The point where the limitation of card sales data appears most clearly is analysis of foreign consumer patterns. Spending by foreign tourists includes not only card payments but also high proportions of cash and mobile app payments such as PayPal, and such transactions are not captured in ordinary domestic card data networks. This creates a data blind spot where the actual spending scale and movement routes of foreigners—who account for a major axis of the real market—are omitted. As a result, a reversal phenomenon is emerging in which brands directly responding to customers at points of contact possess far broader and more sophisticated foreign consumer data than public data.

Q. What new analytical method has been introduced to improve the accuracy of retail consulting?

Through telecom data tracking, we analyze one-to-one matches of what time and minute customers stayed at which store and whether actual payment messages occurred. This allows us to draw a complete persona of how customers entered the parking lot, circulated through the mall along what route, and spent their time. Going forward, consulting success or failure will be determined by who can interpret this consumer behavior data more precisely.

Q. What opportunity factors exist in data that is still unexplored in the retail market?

Foreign tourist data is currently the scarcest yet most essential information in the retail market. In districts such as Myeong-dong and Seongsu, where the share of foreign sales is overwhelming, understanding their information acquisition paths and movement patterns is the core of analysis. “Data route pioneering”—tracking paths from the airport inflow stage and conducting integrated analysis of fragmented data by brand—will become a differentiated battleground in retail consulting. Currently, CBRE is assetizing consumer data by region and brand through close collaboration between the consulting and retail teams, and this will become a key driver supporting precise decision-making for all future projects.

The future market’s success or failure will depend on how three-dimensionally fragmented consumer movement paths are interpreted and how precisely data blind spots, such as foreign consumer patterns, are turned into assets. In a changing environment, thorough preparation is needed so that new market opportunities can be preempted through strategic insights aligned with global standards.

Official real estate market data points to shrinking supply and weakened consumption, but the on-the-ground sentiment in practice is different. It is the result of a mix of income structures of individual assets that are not captured in statistics, irregular consumer movement paths, and the distorted vacancy fatigue created by a traditional supplier-centric mindset. So, has the retail market truly reached its end? Or are new opportunities hidden where we have not looked? The current crisis is not a market collapse, but merely an advancement of business formats that demands a sophisticated, data-driven perspective. Through an interview with Deputy Manager Stella Jung of the CBRE Retail Consulting Team, we examine the real reason we must go beyond simple location theory and identify the micro-level competitiveness of individual assets.

Retail Consulting That Designs Purpose

Q. What is the consulting team’s practical role and position in the real estate development process?

Every real estate development begins with setting the purpose of a site before purchasing the land. The consulting team is the department that draws the initial blueprint at this very front stage, then intervenes in the process as constructors and developers join and revenue scale is estimated, laying the groundwork for disposition and leasing. In other words, consulting is the department that first encounters market information and forecasts what development scenarios will unfold ahead.

Q. There are many diagnoses that the retail market is in crisis lately—what is the actual atmosphere felt in the field?

People around us say commercial facilities have failed, but what we feel in the field seems completely different. Sales at major retail assets are currently soaring (including department stores and retail malls), and the “malling” phenomenon—where consumers solve everything from start to finish in one place—is becoming even more evident. In particular, because Korea is heavily affected by seasons and weather, there is a strong tendency to complete all routines inside one building without going outside, and this is proven by the overwhelming performance of large mixed-use shopping malls such as Starfield.

A quiet view inside a retail mall in the morning. After lunchtime, it becomes crowded even on weekdays with nearby residents and visitors.

It’s Not That People Aren’t Spending—It’s Just Polarized

Q. What interesting common pattern was found in the actual movement paths of large shopping mall visitors?

A recent three-month full-scale survey of 600 visitors at a major shopping mall drew a very clear consumer persona. A large share of visitors showed a routine of 반드시 stopping by Daiso and Olive Young when entering or leaving the mall, suggesting that consumers visit malls not only for glamorous shopping but also to satisfy practical daily needs. This also shows the tremendous influence of Daiso and Olive Young, but luxury stores are also performing well, and we can clearly confirm that polarization is deepening.

An Olive Young located inside Lotte World Mall.

Q. How significant is the status of Daiso and Olive Young within retail malls?

Retail trends that were previously encountered only through articles or rumors were fully proven with numerical data through this consumer behavior study. In particular, Daiso demonstrates strong customer-drawing power regardless of nationality in both residential trade areas and tourist districts such as Dongdaemun, serving as a core retail anchor.

The most notable point is Daiso’s cosmetics section. Its popularity is so high that foreign tourists buy products by the box as soon as they are stocked, meaning it now has very high potential to emerge as a strong competitor to Olive Young. A representative case is Zoom by Jung Saem Mool, a Daiso-exclusive line recently launched by JUNGSAEMMOOL Beauty. User reviews are pouring in saying this product line delivers overwhelming quality beyond simple price merit. Since items such as cushion foundations that used to cost in the KRW 40,000 range can be purchased at Daiso for around KRW 5,000, sold-out chaos occurs immediately upon release, to the point that it is hard even to browse products on the shelves.

Daiso cosmetics shelves are filled with a wide variety of cosmetic products.

Q. What pattern does consumer polarization observed in retail assets recently take?

The current retail market is in a state of severe polarization where the middle ground has disappeared. Even looking only at shopping malls, ambiguous luxury brands struggle, while high-end luxury performs above maintenance levels. Even after several price increases, consumers are boldly investing in luxury jewelry and high-priced bags while simultaneously buying low-priced daily necessities at Daiso and getting nail art—showing consumption behavior where they open their wallets intensively only in places that offer clear personal value.

Q. Why do you analyze that department store sales continue to rise beyond the inflation rate?

Because due to consumption polarization, the sales portion from VIP customers remains overwhelmingly dominant. In addition, select shops such as emerging designer brands and Musinsa premium lines have successfully taken hold and are absorbing trend-sensitive demand. Sales growth in the 6% range, exceeding inflation, is the result not merely of price hikes but of the advancement of these high value-added brands and premium food halls.

“Experience in the Mall, Payment on the Phone”: The Lowest-Price Wall Toy Stores Couldn’t Overcome

Q. In kids-targeted spaces, which category is underperforming in sales contrary to expectations?

Common sense suggests that kids cafés or large toy stores would have high sales, but actual data shows otherwise. Parents visit kids floors most frequently with their children and let them experience products, but actual purchases often happen online after searching for the lowest internet price on site, so it does not translate into offline sales. Those raising children may know this even better—the moment kids play with toys is often only that moment. After all, the place where you can hand a child ten thousand won and fill both hands with satisfaction is probably Daiso. Even if there is nearby residential demand, this is why sales at toy-selling facilities are lower than expected.

Q. Then what is the secret of brands that generate overwhelming sales on kids floors?

According to a recent field survey at a shopping mall, New Balance Kids ranked No. 1 in sales on the kids floor. This is because parents and children can share the brand, and functional trust has been secured through products like shoes designed for children’s comfort and activity. The retail winners are no longer spaces only for children, but value-sharing brands where parents’ taste and children’s practicality intersect. Parents and children can match outfits, and they can buy shoes in the same design.

A Generational Shift in Data

Q. What are the limitations of card sales data that has been widely used?

Card sales data has now become so public that even public institutions open it, so it is no longer a differentiated source. Card records only show the result of spending money, and cannot identify behaviors such as entering a store and doing only window shopping without purchasing, or movement paths. It is insufficient for explaining specific causality about where consumers came from and why they came.

The point where the limitation of card sales data appears most clearly is analysis of foreign consumer patterns. Spending by foreign tourists includes not only card payments but also high proportions of cash and mobile app payments such as PayPal, and such transactions are not captured in ordinary domestic card data networks. This creates a data blind spot where the actual spending scale and movement routes of foreigners—who account for a major axis of the real market—are omitted. As a result, a reversal phenomenon is emerging in which brands directly responding to customers at points of contact possess far broader and more sophisticated foreign consumer data than public data.

Q. What new analytical method has been introduced to improve the accuracy of retail consulting?

Through telecom data tracking, we analyze one-to-one matches of what time and minute customers stayed at which store and whether actual payment messages occurred. This allows us to draw a complete persona of how customers entered the parking lot, circulated through the mall along what route, and spent their time. Going forward, consulting success or failure will be determined by who can interpret this consumer behavior data more precisely.

Q. What opportunity factors exist in data that is still unexplored in the retail market?

Foreign tourist data is currently the scarcest yet most essential information in the retail market. In districts such as Myeong-dong and Seongsu, where the share of foreign sales is overwhelming, understanding their information acquisition paths and movement patterns is the core of analysis. “Data route pioneering”—tracking paths from the airport inflow stage and conducting integrated analysis of fragmented data by brand—will become a differentiated battleground in retail consulting. Currently, CBRE is assetizing consumer data by region and brand through close collaboration between the consulting and retail teams, and this will become a key driver supporting precise decision-making for all future projects.

The future market’s success or failure will depend on how three-dimensionally fragmented consumer movement paths are interpreted and how precisely data blind spots, such as foreign consumer patterns, are turned into assets. In a changing environment, thorough preparation is needed so that new market opportunities can be preempted through strategic insights aligned with global standards.

More in

More in

market

market

market

Apr 2, 2026

Office Retail: No Longer the Sidekick

Beyond rental spaces, office retail determines the sophistication of an office.

market

Mar 4, 2026

The reason why choosing a flagship store location based on intuition can lead to disaster.

The 'Golden Rule' for successful location selection proven by data from 31 industry experts.

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam