Back

Copy

Share

Like

market

Office Retail: No Longer the Sidekick

Office Retail: No Longer the Sidekick

Office Retail: No Longer the Sidekick

Office retail started in underground food courts and evolved into destination anchors that attract outside visitors. It is a structural transformation over 15 years. Landlords look at the coherence of the merchandising mix (MD), and tenants negotiate using data. Preferred assets have people lining up, while less preferred assets face worsening vacancies.

Office retail started in underground food courts and evolved into destination anchors that attract outside visitors. It is a structural transformation over 15 years. Landlords look at the coherence of the merchandising mix (MD), and tenants negotiate using data. Preferred assets have people lining up, while less preferred assets face worsening vacancies.

Office retail started in underground food courts and evolved into destination anchors that attract outside visitors. It is a structural transformation over 15 years. Landlords look at the coherence of the merchandising mix (MD), and tenants negotiate using data. Preferred assets have people lining up, while less preferred assets face worsening vacancies.

Article Highlights

"From Appendix to Main Text": Redefining Office Retail

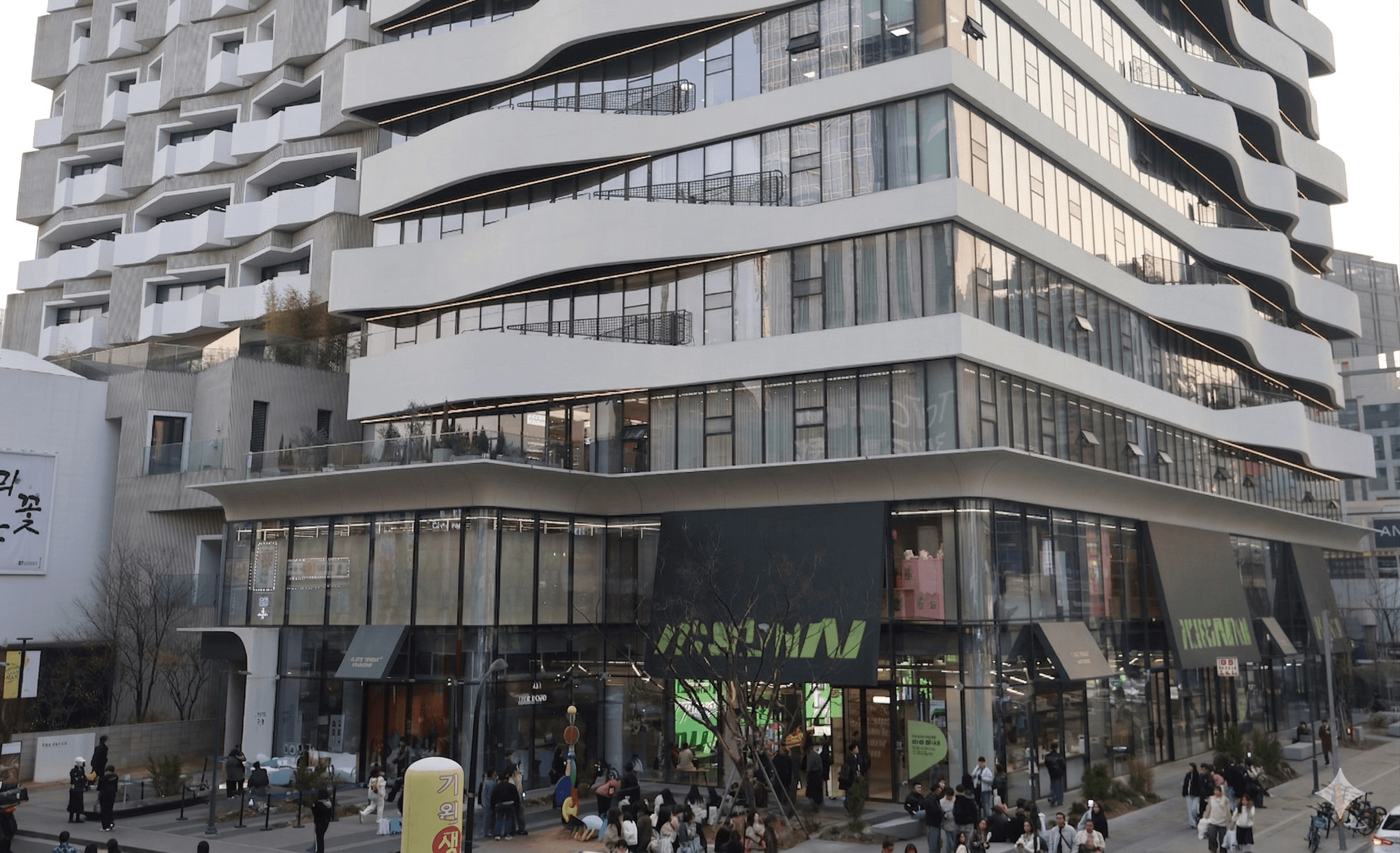

As prime offices such as Center 1 and D Tower strategically place bold retail facades and destination-type tenants on their ground floors, retail has evolved beyond a mere support facility. It has now become a core weapon that defines a building’s grade and justifies its rental premiums.

The Evolution of the "Anchor": Brands Shifting District Flows

As seen in the case of Olive Young N Seongsu, a single unrivaled brand can transform an office building into a premier "hot spot." Retail composition has now entered a stage of strategic capitalization, moving beyond employee welfare to maximize external foot traffic and public engagement.

Operational Expertise as Asset Competitiveness

Amidst the oversupply and polarization of prime offices, sophisticated management models—such as Shinsegae Property’s outsourced operation of Gran Seoul—go beyond simple leasing. These models maintain the building’s prestige and ensure downward rigidity, proving the long-term stability and resilience of the asset.

It’s My Turn to Take the Spotlight

The skyline of Seoul is shifting. In the past, office retail—represented by basement food courts—was merely a secondary space for office workers to grab a quick lunch. Today, however, office retail has rapidly emerged as a key driver that defines a building’s first impression and proves its asset value. Jae-hwang Lee, Associate Director of the CBRE Korea Retail Team, is an expert who has witnessed the dramatic transformation of Seoul’s office market from the front lines over the past 15 years. From iconic landmarks like Center 1 and IFC to the groundbreaking evolution of Olive Young in Seongsu-dong, we explore his diagnosis of the current office retail landscape and its future strategic direction.

1. The Beginning of a Structural Shift

Q. Over the past 15 years, Seoul’s office retail has evolved from mere support facilities into independent commercial entities that define a building’s value. What was the decisive moment that convinced you this shift was a structural transformation rather than a short-term trend?

[The Office as a Destination]

The past 15 years have been a period where the very concept of office retail was redefined. The starting point was the emergence of Center 1 and Ferrum Tower alongside the restoration of Cheonggyecheon. At the time, these two buildings completely shattered the stereotype that basement food courts were spaces reserved only for tenant employees. The sight of crowds flocking to Center 1 on weekends to enjoy brunch at Cafe Mamas (opened in 2011) or coffee at Artisée (opened in 2011), along with the entry of premium dining brands at Ferrum Tower, was the first event to prove that an office building could become a destination for outsiders.

Following this, IFC expanded the possibilities of large-scale commercial infrastructure, while D Tower demonstrated how to elevate a building's sensitivity and prestige through retail facades and terrace spaces. More recently, with cases like Kakao Agit and Tech 1 in Pangyo, retail has evolved to a stage where it forms an ecosystem on a district-wide scale, moving beyond individual buildings.

In particular, the rapid increase in real estate asset management companies and the rise in asset values appear to have accelerated this transformation. As the competition for Value-add intensified, retail evolved beyond a space for collecting rent into the most powerful weapon that determines a building's grade and justifies its rental premiums.

Uniqlo located on the 1st and 2nd floors of D Tower

Q. Are there any specific cases where office retail transformed from serving fixed demand into a space for "destination-based consumption"?

[The Rule Breakers]

If Center 1 opened up the possibilities of office retail, Tesla’s first store at IFC and Uniqlo at D Tower were revolutionary cases that shattered the stereotype of "car showrooms and SPA brands in an office lobby." At the time, the gold standard for car showrooms was a standalone building in specialized districts where import brands clustered. Tesla completely ignored that convention and chose the first floor of a prime office building for its debut.

The current pinnacle of this trend is Olive Young N Seongsu. This store, located in the Factorial Seongsu building, is not just another Olive Young branch. Countless tourists and locals visit Seongsu-dong specifically for this location. It serves as a perfect example of the evolution of an anchor tenant, where a single brand alters the very flow of foot traffic in a district and transforms an office building into a premier "hot spot."

Even on weekday afternoons, OliveYoung N at Factorial Seongsu is bustling with numerous tourists.

2. Regional Retail DNA and Trends

Q. What are the distinct characteristics of office retail across Seoul’s major business districts?

[The Office Retail Landscape]

In YBD (Yeouido) and CBD (Downtown), utilizing in-building retail has now become the standard. Yeouido witnessed explosive growth in its weekend commercial scene following the opening of The Hyundai Seoul, while the CBD has seen high-sensitivity F&B become a part of daily life with the emergence of modern new-builds.

In contrast, GBD (Gangnam) has a physical structure that makes it difficult to form large-scale office retail arcades, as individual floor plates are relatively small. The fact that Teheran-ro is a linear commercial district stretching over a long distance also poses a limit to creating a concentrated cluster effect. However, locations like GFC and Centerfield, which offer parking convenience and pleasant spatial environments, are successfully absorbing the demand for business dining.

Given that these are office districts, a common trait across all three is that high-end business dining—optimized for professional meetings—has taken the place of traditional fine dining. Representative examples include premium Hanwoo (Korean beef) dining centered around private rooms, as well as course-based Korean and Japanese restaurants.

Q. What are the latest trends breaking the old "basement food court" formula?

[The Face of the Building]

The most significant shift is the reduction of physical bank branches and the resulting rise of ground-floor retail. As banks, which were once the most stable tenants, vacate their prime spots, these spaces are being filled by brands and large-scale cafes that serve as the "face" of the building.

Furthermore, there is a clear trend of vertically expanding retail space from the ground floor to the upper levels. Retail is no longer hidden in the basement; it has boldly moved to the forefront, acting as a show window that defines the building’s first impression.

Starbucks Reserve, located on the first floor of the KT WEST building, is busy with tourists and office workers nearby.

3. The Dynamics Between Landlord and Tenant

Q. What conditions are landlords currently more sensitive to than rent?

[Fit & Sustainability]

Rent is the baseline, but the alignment of the tenant mix (MD) has become a higher priority. Landlords meticulously evaluate whether a brand’s "prestige" fits the building's office tenants and whether the company has the high creditworthiness to eliminate the risk of mid-term termination. Furthermore, a key evaluation factor is whether a tenant can form a peer group that maintains and enhances the building's overall value.

Q. How should the exit risk of an anchor tenant be managed?

[Matching the right one]

The departure of an anchor can be a crisis, but the "manner" of the exit is what matters. If a tenant vacates for expansion, that space is already a proven "prime spot," allowing the landlord to attract a new tenant under even better conditions. However, if the location is ambiguous or the brand has declined, professional solutions are required.

In the case of Twin Tree Tower, the space wasn't simply replaced; the retail identity was redefined by restructuring the spatial layout through a major renovation. The utility of the space was then perfected when a brand like Szimpatikus moved in. Similarly, Louvre Baguette at Gran Seoul’s Pimat-gil is an example of content perfectly tailored to its location. Ultimately, the core is the compatibility between space and content, and matching the two is the essential role of the CBRE Retail Team.

France Louvre Baguette located on the first floor of Grand Seoul. During the 'Ddujeonku' craze, there was even a waiting line outside the store due to its popularity.

4. New Supply and Market Restructuring

Q. How will the emergence of large-scale new-build offices affect the retail spaces of existing older buildings?

[Expand & Cluster]

I view this not as a zero-sum game, but as an opportunity for market expansion. When a new-build office enters the scene, it triggers a clustering effect that grows the surrounding commercial district together. As seen in the KT West–D Tower–Gran Seoul axis in Gwanghwa-mun or the The Hyundai–IFC–One Sentinel axis in Yeouido, when retail flow connects to form a "belt," the influx of outside visitors multiplies.

In this process, well-prepared older buildings can actually solidify their asset value by benefiting from the trickle-down effect of the new developments. They maintain their status as "must-enter" buildings for brands, even as specific tenants rotate. For an office landlord, this is the most critical factor—whether the building itself has been "branded." Conversely, buildings without a distinct identity will fall behind in the competition with new-builds, further intensifying the polarization of the market.

D Tower SOHO

Starfield Grand Seoul, visible in the front

The interior of KT WEST, which recently completed renovations.

'Oats Coffee', which recently opened a store in Paris to showcase K-Coffee, is also located on the 2nd floor of KT WEST.

The café space and office lobby serve as a waiting area and meeting space for office visitors.

Q. In the Seoul market, where prime office vacancy rates are low, how are actual retail lease terms (rent, TI, etc.) evolving?

[The Polarization of Assets]

Even within the same district, there is a stark difference in "temperature" between assets. A strange phenomenon is occurring where landlords of preferred assets can afford to hand-pick their brands, while non-preferred assets struggle with retail vacancies even when their office floors are fully occupied.

Tenants today are often better informed about market data than landlords. They directly verify actual sales data from neighboring stores and frequently check for the feasibility of daytime construction to reduce labor costs and TI (Tenant Improvement) expenditure. Furthermore, unlike when entering traditional department stores, tenants in office buildings are now aggressively demanding signage rights and external facade exposure to clearly project their brand identity.

While tenants' demands for support have increased due to the recent surge in construction costs, existing fund-owned assets—unlike new supply—face structural difficulties in allocating additional budgets. Because their budgets are often tightly set from the time of acquisition, executing additional construction expenses during the operational phase remains a significant challenge.

Q. We are seeing an increase in cases where office retail is managed through master leases by major asset management firms or retail conglomerates. What is your perspective on this?

[The Dilemma of Profit vs. Risk]

To be blunt, there have been very few models of past office retail master leases that could be evaluated as truly successful. Looking back, I believe the biggest failure was a complacent "copy and paste" approach. By chasing efficiency and planting identical tenant mixes (MD) across various buildings, the scarcity and unique character that an individual asset should possess were diluted.

However, the more fundamental issue lies in the misalignment of interests between the landlord and the operator. Operators sometimes sublease at low rates or attract brands that do not fit the building's prestige simply to fill vacancies. From the landlord's perspective, this creates a vicious cycle: "I outsourced management to increase my building's value, but it's being eroded by low-end brands." Furthermore, because the landlord's actual net income structurally decreases while commission costs rise, the math rarely adds up for a typical asset.

That said, the recent case of Shinsegae Property managing Gran Seoul has a slightly different nuance. This appears to be a bold strategic investment where the landlord chose "maintenance of building grade" and operational expertise over immediate profit maximization. To compete with neighboring D Tower and other new-builds, they opted to "borrow" overwhelming operational capabilities despite the costs.

Consequently, I believe this is a highly sophisticated and specialized model that can only be selected by prime buildings capable of making bold large-scale investment decisions, or headquarters-type assets where symbolism outweighs profitability. While I have high expectations for this case, I find it difficult to see it being broadly applied to general office retail.

The 4th floor of Gran Seoul is filled with brands optimized for business dining and formal meetings, breaking away from the typical restaurant vibe.

5. The Near Future of Office Retail

Q. Do you believe that retail tenant mix (MD) directly contributes to the upper-floor office rents (NOC) and asset value (Cap Rate) beyond simply expanding amenities?

[Yes and Yes]

I personally experienced the leasing competition between IFC and FKI in YBD during the mid-2010s. At that time, it didn't feel as though differences in retail composition translated into immediate rent gaps. The office market was exceptionally strong, and the hardware specifications appeared quite similar.

However, over time, those small differences revealed a distinct gap in asset competitiveness. While IFC possessed powerful hardware—such as subway connectivity and hotel integration—it was the abundant internal F&B and ideally accessible Daily MD that ultimately completed that hardware.

Because tenants are not just leasing office space but choosing the infrastructure their employees will enjoy, a building with strong retail gains a powerful justification to demand higher NOC (Net Occupancy Cost) compared to surrounding market rates.

When retail is excellent—particularly when Daily MD outperforms business dining—tenant preference is overwhelmingly higher. Even during downturns or periods of oversupply, buildings with solid retail see less tenant churn. I believe this downward rigidity serves as clear proof of an asset's stability.

Q. What is the most ideal form of a landmark office in Seoul?

The most ideal form of an office building, in my view, is one where ground-level profitability and overwhelming subterranean scale coexist.

Ground Floor: Boldly conceding the first floor to retail to secure a wide, horizontal facade. This transforms the entire building into a massive Brand Wall, injecting commercial vitality into the streetscape.

Subterranean Lobby: Moving the lobby underground while maximizing ceiling heights and placing luxury amenities. This provides an overwhelming spatial experience, making visitors feel as if they are entering a "new realm" rather than a basement.

Retail: Implementing targeted curation that reflects the context of the surrounding district. This creates a "living landmark" that brands compete to enter, even as time passes.

Retail on the first floor, with office lobbies on the underground floor (image created by AI for understanding).

Q. A large-scale supply of prime office space is scheduled for Seoul over the next two years. What strategic preparations is the CBRE Retail Team making for these upcoming market changes?

[Back to Basics]

While a large-scale supply of office space is scheduled to begin in 2029, we are focusing on the essence of providing excellent service to our clients rather than grand future strategies. By executing major projects such as TP Tower in 2024, One Grove in 2025, and 63 Building in Yeouido in 2026, we are building our expertise on the ground every single day.

Our greatest strength and the key differentiator from other retail consultancies lies in our "One Team" spirit. Five specialized teams within our retail division collaborate organically to provide optimal solutions for both landlords and tenants. Our assets include extensive experience and data spanning from emerging markets like Seongsu and Dosan to traditional CBD and GBD districts. I am confident that staying faithful to our current tasks and building trust will be the most unshakable competitive advantage in the upcoming era of massive supply.

Office retail has now moved beyond being a mere support facility for tenants to become a core driver that defines a building's identity and propels its asset value. As Associate Director Jae-hwang Lee emphasized, this is not a passing fad but a massive structural shift in Seoul’s commercial real estate market. In the face of the upcoming large-scale supply and market polarization, the ultimate factor determining success will be the power of the content that fills the space and the expertise used to operate it.

It’s My Turn to Take the Spotlight

The skyline of Seoul is shifting. In the past, office retail—represented by basement food courts—was merely a secondary space for office workers to grab a quick lunch. Today, however, office retail has rapidly emerged as a key driver that defines a building’s first impression and proves its asset value. Jae-hwang Lee, Associate Director of the CBRE Korea Retail Team, is an expert who has witnessed the dramatic transformation of Seoul’s office market from the front lines over the past 15 years. From iconic landmarks like Center 1 and IFC to the groundbreaking evolution of Olive Young in Seongsu-dong, we explore his diagnosis of the current office retail landscape and its future strategic direction.

1. The Beginning of a Structural Shift

Q. Over the past 15 years, Seoul’s office retail has evolved from mere support facilities into independent commercial entities that define a building’s value. What was the decisive moment that convinced you this shift was a structural transformation rather than a short-term trend?

[The Office as a Destination]

The past 15 years have been a period where the very concept of office retail was redefined. The starting point was the emergence of Center 1 and Ferrum Tower alongside the restoration of Cheonggyecheon. At the time, these two buildings completely shattered the stereotype that basement food courts were spaces reserved only for tenant employees. The sight of crowds flocking to Center 1 on weekends to enjoy brunch at Cafe Mamas (opened in 2011) or coffee at Artisée (opened in 2011), along with the entry of premium dining brands at Ferrum Tower, was the first event to prove that an office building could become a destination for outsiders.

Following this, IFC expanded the possibilities of large-scale commercial infrastructure, while D Tower demonstrated how to elevate a building's sensitivity and prestige through retail facades and terrace spaces. More recently, with cases like Kakao Agit and Tech 1 in Pangyo, retail has evolved to a stage where it forms an ecosystem on a district-wide scale, moving beyond individual buildings.

In particular, the rapid increase in real estate asset management companies and the rise in asset values appear to have accelerated this transformation. As the competition for Value-add intensified, retail evolved beyond a space for collecting rent into the most powerful weapon that determines a building's grade and justifies its rental premiums.

Uniqlo located on the 1st and 2nd floors of D Tower

Q. Are there any specific cases where office retail transformed from serving fixed demand into a space for "destination-based consumption"?

[The Rule Breakers]

If Center 1 opened up the possibilities of office retail, Tesla’s first store at IFC and Uniqlo at D Tower were revolutionary cases that shattered the stereotype of "car showrooms and SPA brands in an office lobby." At the time, the gold standard for car showrooms was a standalone building in specialized districts where import brands clustered. Tesla completely ignored that convention and chose the first floor of a prime office building for its debut.

The current pinnacle of this trend is Olive Young N Seongsu. This store, located in the Factorial Seongsu building, is not just another Olive Young branch. Countless tourists and locals visit Seongsu-dong specifically for this location. It serves as a perfect example of the evolution of an anchor tenant, where a single brand alters the very flow of foot traffic in a district and transforms an office building into a premier "hot spot."

Even on weekday afternoons, OliveYoung N at Factorial Seongsu is bustling with numerous tourists.

2. Regional Retail DNA and Trends

Q. What are the distinct characteristics of office retail across Seoul’s major business districts?

[The Office Retail Landscape]

In YBD (Yeouido) and CBD (Downtown), utilizing in-building retail has now become the standard. Yeouido witnessed explosive growth in its weekend commercial scene following the opening of The Hyundai Seoul, while the CBD has seen high-sensitivity F&B become a part of daily life with the emergence of modern new-builds.

In contrast, GBD (Gangnam) has a physical structure that makes it difficult to form large-scale office retail arcades, as individual floor plates are relatively small. The fact that Teheran-ro is a linear commercial district stretching over a long distance also poses a limit to creating a concentrated cluster effect. However, locations like GFC and Centerfield, which offer parking convenience and pleasant spatial environments, are successfully absorbing the demand for business dining.

Given that these are office districts, a common trait across all three is that high-end business dining—optimized for professional meetings—has taken the place of traditional fine dining. Representative examples include premium Hanwoo (Korean beef) dining centered around private rooms, as well as course-based Korean and Japanese restaurants.

Q. What are the latest trends breaking the old "basement food court" formula?

[The Face of the Building]

The most significant shift is the reduction of physical bank branches and the resulting rise of ground-floor retail. As banks, which were once the most stable tenants, vacate their prime spots, these spaces are being filled by brands and large-scale cafes that serve as the "face" of the building.

Furthermore, there is a clear trend of vertically expanding retail space from the ground floor to the upper levels. Retail is no longer hidden in the basement; it has boldly moved to the forefront, acting as a show window that defines the building’s first impression.

Starbucks Reserve, located on the first floor of the KT WEST building, is busy with tourists and office workers nearby.

3. The Dynamics Between Landlord and Tenant

Q. What conditions are landlords currently more sensitive to than rent?

[Fit & Sustainability]

Rent is the baseline, but the alignment of the tenant mix (MD) has become a higher priority. Landlords meticulously evaluate whether a brand’s "prestige" fits the building's office tenants and whether the company has the high creditworthiness to eliminate the risk of mid-term termination. Furthermore, a key evaluation factor is whether a tenant can form a peer group that maintains and enhances the building's overall value.

Q. How should the exit risk of an anchor tenant be managed?

[Matching the right one]

The departure of an anchor can be a crisis, but the "manner" of the exit is what matters. If a tenant vacates for expansion, that space is already a proven "prime spot," allowing the landlord to attract a new tenant under even better conditions. However, if the location is ambiguous or the brand has declined, professional solutions are required.

In the case of Twin Tree Tower, the space wasn't simply replaced; the retail identity was redefined by restructuring the spatial layout through a major renovation. The utility of the space was then perfected when a brand like Szimpatikus moved in. Similarly, Louvre Baguette at Gran Seoul’s Pimat-gil is an example of content perfectly tailored to its location. Ultimately, the core is the compatibility between space and content, and matching the two is the essential role of the CBRE Retail Team.

France Louvre Baguette located on the first floor of Grand Seoul. During the 'Ddujeonku' craze, there was even a waiting line outside the store due to its popularity.

4. New Supply and Market Restructuring

Q. How will the emergence of large-scale new-build offices affect the retail spaces of existing older buildings?

[Expand & Cluster]

I view this not as a zero-sum game, but as an opportunity for market expansion. When a new-build office enters the scene, it triggers a clustering effect that grows the surrounding commercial district together. As seen in the KT West–D Tower–Gran Seoul axis in Gwanghwa-mun or the The Hyundai–IFC–One Sentinel axis in Yeouido, when retail flow connects to form a "belt," the influx of outside visitors multiplies.

In this process, well-prepared older buildings can actually solidify their asset value by benefiting from the trickle-down effect of the new developments. They maintain their status as "must-enter" buildings for brands, even as specific tenants rotate. For an office landlord, this is the most critical factor—whether the building itself has been "branded." Conversely, buildings without a distinct identity will fall behind in the competition with new-builds, further intensifying the polarization of the market.

D Tower SOHO

Starfield Grand Seoul, visible in the front

The interior of KT WEST, which recently completed renovations.

'Oats Coffee', which recently opened a store in Paris to showcase K-Coffee, is also located on the 2nd floor of KT WEST.

The café space and office lobby serve as a waiting area and meeting space for office visitors.

Q. In the Seoul market, where prime office vacancy rates are low, how are actual retail lease terms (rent, TI, etc.) evolving?

[The Polarization of Assets]

Even within the same district, there is a stark difference in "temperature" between assets. A strange phenomenon is occurring where landlords of preferred assets can afford to hand-pick their brands, while non-preferred assets struggle with retail vacancies even when their office floors are fully occupied.

Tenants today are often better informed about market data than landlords. They directly verify actual sales data from neighboring stores and frequently check for the feasibility of daytime construction to reduce labor costs and TI (Tenant Improvement) expenditure. Furthermore, unlike when entering traditional department stores, tenants in office buildings are now aggressively demanding signage rights and external facade exposure to clearly project their brand identity.

While tenants' demands for support have increased due to the recent surge in construction costs, existing fund-owned assets—unlike new supply—face structural difficulties in allocating additional budgets. Because their budgets are often tightly set from the time of acquisition, executing additional construction expenses during the operational phase remains a significant challenge.

Q. We are seeing an increase in cases where office retail is managed through master leases by major asset management firms or retail conglomerates. What is your perspective on this?

[The Dilemma of Profit vs. Risk]

To be blunt, there have been very few models of past office retail master leases that could be evaluated as truly successful. Looking back, I believe the biggest failure was a complacent "copy and paste" approach. By chasing efficiency and planting identical tenant mixes (MD) across various buildings, the scarcity and unique character that an individual asset should possess were diluted.

However, the more fundamental issue lies in the misalignment of interests between the landlord and the operator. Operators sometimes sublease at low rates or attract brands that do not fit the building's prestige simply to fill vacancies. From the landlord's perspective, this creates a vicious cycle: "I outsourced management to increase my building's value, but it's being eroded by low-end brands." Furthermore, because the landlord's actual net income structurally decreases while commission costs rise, the math rarely adds up for a typical asset.

That said, the recent case of Shinsegae Property managing Gran Seoul has a slightly different nuance. This appears to be a bold strategic investment where the landlord chose "maintenance of building grade" and operational expertise over immediate profit maximization. To compete with neighboring D Tower and other new-builds, they opted to "borrow" overwhelming operational capabilities despite the costs.

Consequently, I believe this is a highly sophisticated and specialized model that can only be selected by prime buildings capable of making bold large-scale investment decisions, or headquarters-type assets where symbolism outweighs profitability. While I have high expectations for this case, I find it difficult to see it being broadly applied to general office retail.

The 4th floor of Gran Seoul is filled with brands optimized for business dining and formal meetings, breaking away from the typical restaurant vibe.

5. The Near Future of Office Retail

Q. Do you believe that retail tenant mix (MD) directly contributes to the upper-floor office rents (NOC) and asset value (Cap Rate) beyond simply expanding amenities?

[Yes and Yes]

I personally experienced the leasing competition between IFC and FKI in YBD during the mid-2010s. At that time, it didn't feel as though differences in retail composition translated into immediate rent gaps. The office market was exceptionally strong, and the hardware specifications appeared quite similar.

However, over time, those small differences revealed a distinct gap in asset competitiveness. While IFC possessed powerful hardware—such as subway connectivity and hotel integration—it was the abundant internal F&B and ideally accessible Daily MD that ultimately completed that hardware.

Because tenants are not just leasing office space but choosing the infrastructure their employees will enjoy, a building with strong retail gains a powerful justification to demand higher NOC (Net Occupancy Cost) compared to surrounding market rates.

When retail is excellent—particularly when Daily MD outperforms business dining—tenant preference is overwhelmingly higher. Even during downturns or periods of oversupply, buildings with solid retail see less tenant churn. I believe this downward rigidity serves as clear proof of an asset's stability.

Q. What is the most ideal form of a landmark office in Seoul?

The most ideal form of an office building, in my view, is one where ground-level profitability and overwhelming subterranean scale coexist.

Ground Floor: Boldly conceding the first floor to retail to secure a wide, horizontal facade. This transforms the entire building into a massive Brand Wall, injecting commercial vitality into the streetscape.

Subterranean Lobby: Moving the lobby underground while maximizing ceiling heights and placing luxury amenities. This provides an overwhelming spatial experience, making visitors feel as if they are entering a "new realm" rather than a basement.

Retail: Implementing targeted curation that reflects the context of the surrounding district. This creates a "living landmark" that brands compete to enter, even as time passes.

Retail on the first floor, with office lobbies on the underground floor (image created by AI for understanding).

Q. A large-scale supply of prime office space is scheduled for Seoul over the next two years. What strategic preparations is the CBRE Retail Team making for these upcoming market changes?

[Back to Basics]

While a large-scale supply of office space is scheduled to begin in 2029, we are focusing on the essence of providing excellent service to our clients rather than grand future strategies. By executing major projects such as TP Tower in 2024, One Grove in 2025, and 63 Building in Yeouido in 2026, we are building our expertise on the ground every single day.

Our greatest strength and the key differentiator from other retail consultancies lies in our "One Team" spirit. Five specialized teams within our retail division collaborate organically to provide optimal solutions for both landlords and tenants. Our assets include extensive experience and data spanning from emerging markets like Seongsu and Dosan to traditional CBD and GBD districts. I am confident that staying faithful to our current tasks and building trust will be the most unshakable competitive advantage in the upcoming era of massive supply.

Office retail has now moved beyond being a mere support facility for tenants to become a core driver that defines a building's identity and propels its asset value. As Associate Director Jae-hwang Lee emphasized, this is not a passing fad but a massive structural shift in Seoul’s commercial real estate market. In the face of the upcoming large-scale supply and market polarization, the ultimate factor determining success will be the power of the content that fills the space and the expertise used to operate it.

More in

More in

market

market

market

Mar 4, 2026

The reason why choosing a flagship store location based on intuition can lead to disaster.

The 'Golden Rule' for successful location selection proven by data from 31 industry experts.

market

Mar 8, 2026

A two-year tragedy tied up in permits and approvals—your brand must be different.

CBRE Retail-TNT's one-stop solution enables seamless global expansion.

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam