Back

Copy

Share

Like

market

The End of Commercial Complexes

The End of Commercial Complexes

The End of Commercial Complexes

공식 통계가 잡지 못하는 숨은 공급이 분양상가 시장을 과포화 상태로 몰아가고 있다. PF 구조의 모순 속에서도 앵커 테넌트와 마이크로 기획이 검증된 자산은 여전히 생존한다.

공식 통계가 잡지 못하는 숨은 공급이 분양상가 시장을 과포화 상태로 몰아가고 있다. PF 구조의 모순 속에서도 앵커 테넌트와 마이크로 기획이 검증된 자산은 여전히 생존한다.

공식 통계가 잡지 못하는 숨은 공급이 분양상가 시장을 과포화 상태로 몰아가고 있다. PF 구조의 모순 속에서도 앵커 테넌트와 마이크로 기획이 검증된 자산은 여전히 생존한다.

Article Highlights

데이터가 가린 과공급의 진실: 공식 지표상 공급은 줄었으나, 지식산업센터와 주상복합 등 통계 외 변칙적 공급과 PF 구조에 매몰된 선분양 방식이 역대급 공실 피로감을 만들었다.

매크로 분석에서 마이크로 기획으로: 상권 전체의 부활을 기다리기보다 개별 건물의 수직 동선, 주차 편의성 등 물리적 경쟁력을 정밀 진단하여 '적자생존'하는 마이크로 상품 기획이 필수적이다.

자산 가치를 결정하는 앵커 테넌트의 힘: 스타벅스 같은 우량 브랜드는 단순 임대 수익을 넘어 상권의 좌표를 찍고 금융권 신뢰도(RTI)를 높여 자산의 환금성을 보장하는 핵심 보증수표가 된다.

Cold Wind Blowing Distribution Retail Space

Official data indicates a reduction in supply, but the field is suffering from unprecedented vacancy fatigue. The irregular supply of knowledge industry centers and mixed-use developments that do not show up in statistics, along with a Korean-style PF structure focused solely on sales profits, have resulted in a distorted outcome. Does this mean that distribution retail spaces can no longer serve as investment vehicles? Or is it that distribution retail spaces now have no place? As housing regulations tighten, retail spaces continue to be an attractive investment that generates cash flow, and the current crisis is merely a transition requiring a heightened perspective on market realities. Through the analysis provided by Ji-Sun Myung, Senior Managing Director of CBRE's Retail Team, we explore the real reasons why we need to identify the micro competitiveness of individual buildings rather than relying on simplistic analyses and basic location theories, and prepare for the future.

The Truth About Oversupply Hidden by Statistics: The Traps of PF

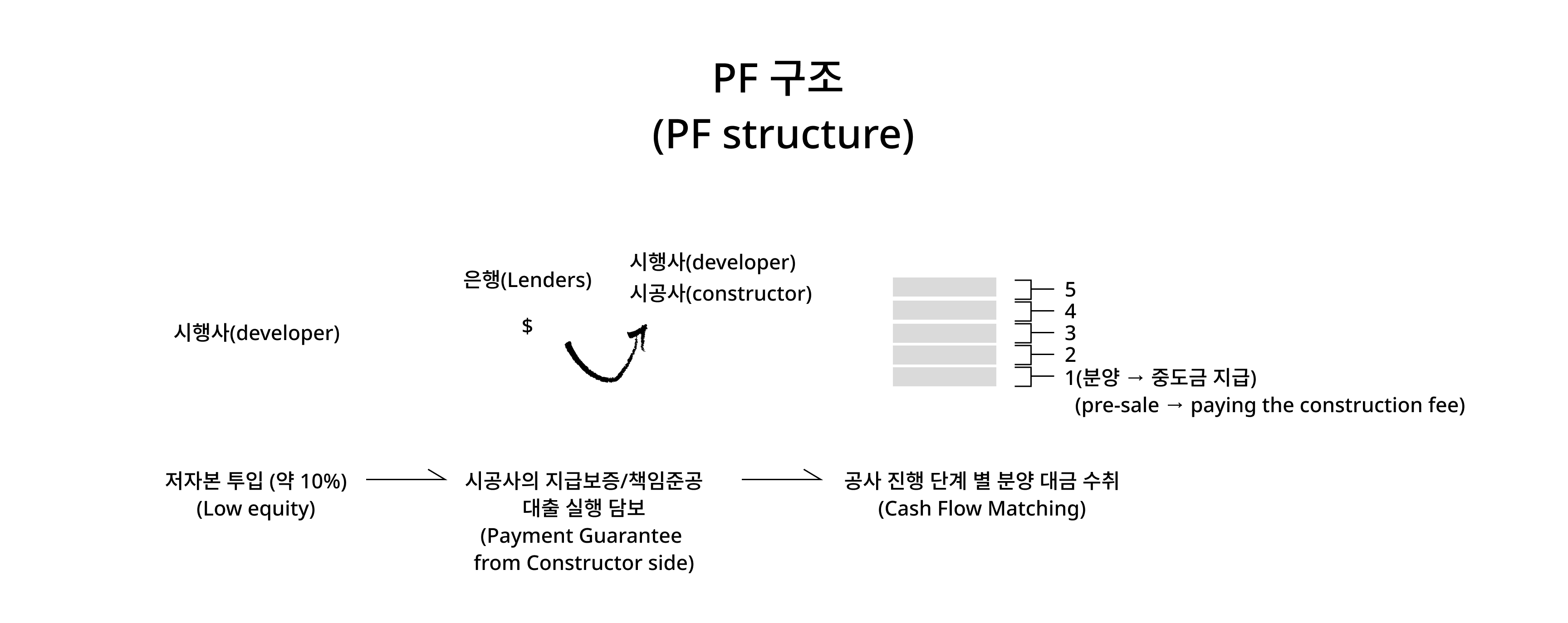

The official data in the real estate market states that the supply of commercial land is decreasing, but the on-site temperature feels different. If past commercial supply was limited to planned 'central commercial areas', recently, we have seen an explosion of supply occurring in irregular manners that do not show up in the data, such as lower levels of knowledge industry centers, mixed-use developments (C-Block), and cafe streets in relocation areas.

This oversupply is rooted in the uniquely Korean PF (Project Financing) structure. Developers and construction companies must create cash flow throughout the construction period to offset low equity risks, which leads them to adopt the method of pre-selling retail space. Consequently, regardless of market demand, the structural contradiction of retail spaces flooding the market according to construction progress schedules has accumulated vacancy fatigue.

Q. Why have distribution retail spaces thrived in South Korea?

The reason for the prevalence of distribution retail spaces in the South Korean retail market is a combination of the inevitability of the development structure and the unique psychology of asset ownership in Korea. It can be summarized from two main perspectives.

1. Structural Factors of the Development Process: Risk Diversification and Early Cash Flow Acquisition

Firstly, domestic real estate development generally proceeds through PF (Project Financing) based on minimal equity. From the perspective of developers and construction companies, they must settle massive construction and project costs within the 4 to 5 years of construction, making pre-selling retail spaces to recover interim payments the most efficient funding method. In other words, distribution retail spaces were utilized as a key device to diversify the development project's risks and secure cash flow.

2. The Psychology of Physical Asset Ownership: Capital Gains Overwhelming Yield

Another reason is the strong investment psychology towards physical asset ownership. South Korean investors have a very high preference for securing individual ownership rights, including land shares. Particularly in core locations like Gangnam, even though rental yields drop below 2%, which is irrational in terms of operational efficiency, the symbolic nature of owning a shop in Gangnam and expectations for land price increases have driven investment. The psychology that values capital gains over yields has also played a role in sustaining the distribution retail space market.

Q. Why, despite stable supply indicators, is the field experiencing the highest level of vacancy fatigue ever?

1. The Pitfalls of Data: The Terrifying 'Hidden Supply'

First, while the official supply indicators for commercial land maintain levels similar to the past, the market's perception of vacancy fatigue is at an all-time high. This is due to irregular supply occurring in the blind spots of statistics. Although the total amount of designated 'central commercial land' is limited, the actual market has been flooded with retail spaces within residential projects, retail below officetels, and support facilities within knowledge industry centers, particularly the recent culprits of oversupply.

2. The Combined Effect of High Interest Rates and Declining Consumer Spending: 'Arteriosclerosis' of Local Businesses

The combination of oversupply and high-interest rates, along with weakened domestic demand, has completely drained the survival capability of local businesses. As the burdens of principal and interest payments become unbearable for investors and tenants face declining sales, the fatigue accumulates, and local businesses outside the key areas of Seoul are effectively at risk of 'shutdown'.

3. Polarization of Consumer Patterns: The Disappearance of 'Convenient Businesses'

The accumulated fatigue has changed consumer behavior patterns. Now, even with an abundance of liquidity, consumers do not shop at the 'convenient businesses' located at their doorstep or directly beneath their offices. Instead, they gravitate towards certain 'destination retail' businesses that offer clear experiences and content, leading to a fixation on this trend.

4. The Disappearance of Investment Psychology: The Reality of Yield Collapse

Currently, the retail investment market has moved beyond simple contraction to a stage where the psychology itself has vanished. In a situation where yields are not justified, fears of asset value decline dominate the market, creating a significant risk of an overall liquidity crisis in real estate assets.

From Macro Analysis to Micro Planning

In an era where the pie of retail space is shrinking, the existing broad analysis approach becomes pointless. We must abandon the macro perspective that treats the entire retail environment as a single entity and focus on detailed 'micro product planning' that closely examines the functions and competitiveness of individual buildings.

Especially in local metropolitan areas where the risk of population decline has materialized, rather than hope for an overall recovery of the retail space, we need to view our buildings as independent products and devise a 'survival of the fittest' strategy. While the sector may shrink, it will not disappear, so only those buildings that secure definitive functional advantages within the reduced pie will survive.

Category

Macro Approach (Past)

Micro Planning (Present)

Target of Analysis

Overall foot traffic in the retail sector and backing households

Vertical circulation and unit competitiveness of individual buildings

Core Strategy

Filling by product type (Quantity)

Positioning based on functionality (Quality)

Solutions

Attracting tenants through rent adjustments

Re-evaluating asset value through Value-Add

Q. What indicators do you consider most important when diagnosing local retail projects?

1. Precise Diagnosis

In local retail areas, the physical competitiveness of the assets, rather than external inflows, determines success or failure. Therefore, before examining the overall flow of the retail sector, we must first analyze the micro elements of the hardware, checking if the building's circulation is not closed off, and if accessibility from the underground parking lot to the store is effective, as these aspects will help assess the asset's self-sustaining capability and potential.

2. Quality Control

Simply segmenting units to fill vacancies with low-performing industries (such as real estate, mobile phone stores, etc.) may be advantageous for short-term exits, but it destroys the building's longevity and asset value. A thorough investigation must be conducted to ensure that tenants are continuing normal operations within the boundaries of their rent resistance and that they are high-quality tenants paying reasonable rents in line with the market. This information will be foundational for renovations.

3. Feasibility Review of Strategies

Even the optimal strategy proposed by consultants is useless if it lacks the rental capacity to be implemented. A detailed check of the willingness for hardware investment for building improvements, as well as the financial capacity to manage rent adjustments or promotional costs, must be done beforehand. Prioritizing the client's needs while finding feasible 'compromises' within realistic constraints is the essence of practical planning.

4. Professional Approach for the Sustainability of Distribution Retail Spaces

In the case of local distribution retail spaces, complex issues such as adjusting interests with individual owners are prevalent. Thus, a specialized and multifaceted consulting approach that can maintain the asset’s value in the long term is essential, going beyond simple leasing.

Deriving Realistic Compromises for Sustainable MD Configuration

One of the causes undermining asset longevity is the distorted supply structure driven by maximizing sales profits. Developers may unjustifiably split retail spaces to justify high selling prices or fill MDs only with properties that can afford high rents, such as real estate or mobile phone agencies, disregarding the context of the retail environment.

This fragmentation of space and qualitative degradation of tenants ultimately causes the loss of the asset's attracting power, blocking any future efforts for consolidated management or value enhancement.

Q. What argument do you use to persuade clients in a market situation with strong rent resistance?

Tenants are knowledgeable about data and sensitive to market prices. It’s a market where tenants hold the upper hand, and flattery won’t work. Hence, while maintaining face rent, it is necessary to adopt a technical approach that utilizes promotional costs like rent-free periods or interior support (TI) to ease tenants' initial burdens.

Q. Why are anchor tenants like Starbucks or Paul Bassett important?

1. The Trickling Effect of Attraction and Establishing Coordinates in the Retail Sector

Anchor tenants serve the role of establishing what we call 'coordinates' for the building. Brands like Starbucks or Paul Bassett become powerful destinations themselves, drawing in external foot traffic. While they might require sales-based commissions or low rent, resulting in lower short-term profitability, the attracting power they create becomes a decisive catalyst for renting out the remaining small MD units.

2. Trustworthiness from the Financial Sector and Core Variables for RTI Evaluation

When calculating the key indicator for commercial real estate loans, RTI (Rent To Interest), having a high-quality entity like Starbucks within the premises increases the stability and sustainability of rental income, leading to a favorable assessment.

RTI Criterion: For non-residential (commercial) properties, meeting an RTI of 1.5 times or more is necessary to facilitate loans (based on current financial sector guidelines).

Increase in Collateral Value: Retail spaces inhabited by high-quality brands are categorized as 'creditworthy assets' by financial institutions, placing them in advantageous positions regarding loan-to-value (LTV) ratio or interest conditions.

3. Securing Saleability and Ensuring Liquidity for Exit

For developers, the mere title of 'anticipated tenant of Starbucks' becomes a powerful sales marketing tool, and for sub-buyers, it offers a guarantee for high liquidity based on stable operations without worrying about vacancies, enabling them to realize capital gains.

The Essence of Retail Does Not Change

While the crisis discourse surrounding retail is prevalent, it should be interpreted not as the end of the industry but as 'a transition in business formats'. Even if large supermarkets face crises, warehouse models like Costco or E-Mart Traders, or online-integrated models like SSG take the lead in the market. As housing regulations tighten and the desire for cash flow for retirement grows, retail spaces remain attractive investment opportunities. However, a heightened perception is now required—one that invests in proven products rather than merely making investments based on blueprints.

Q. Where are the positive signals for the future of retail investment?

Consistent income of 1 to 2 million won makes retail spaces the most attractive investment option. The inherent value of being able to generate cash flow while avoiding risks from housing regulations remains valid. However, the era of simply building and selling is over. The market will be restructured not merely by 'location' but by execution capabilities such as the following:

Redefining the Purpose of Space: It is essential to clearly define what function (Hub) the building will perform within the community, going beyond simply filling product types.

Value Management Period (Asset Management): Moving away from the mindset that 'exit' happens once a sale is made post-distribution, the ability to maintain tenant sustainability and increase asset value during operational phases will be crucial for investment success.

Data-Based Precise Targeting: The market will only survive through product planning that microscopically analyzes the lifestyle of core targets that actually open their wallets, without being bogged down by macro foot traffic figures.

Ultimately, what we need now is the ability to identify 'real products'. As seen in the case of Gwanggyo El Port, when meticulous MD management by developers harmonizes with appropriate tenant placement, asset value will finally be realized.

I believe that now, when the market has cooled down, is an opportunity to focus on fundamentals. It is not that all retail spaces are sinking into an abyss of vacancies; rather, it is the time to transform with more sophisticated functions and refined retail strategies. As players in the distribution market, we must uncover sustainable content and maintain it consistently to prove 'true value'.

Cold Wind Blowing Distribution Retail Space

Official data indicates a reduction in supply, but the field is suffering from unprecedented vacancy fatigue. The irregular supply of knowledge industry centers and mixed-use developments that do not show up in statistics, along with a Korean-style PF structure focused solely on sales profits, have resulted in a distorted outcome. Does this mean that distribution retail spaces can no longer serve as investment vehicles? Or is it that distribution retail spaces now have no place? As housing regulations tighten, retail spaces continue to be an attractive investment that generates cash flow, and the current crisis is merely a transition requiring a heightened perspective on market realities. Through the analysis provided by Ji-Sun Myung, Senior Managing Director of CBRE's Retail Team, we explore the real reasons why we need to identify the micro competitiveness of individual buildings rather than relying on simplistic analyses and basic location theories, and prepare for the future.

The Truth About Oversupply Hidden by Statistics: The Traps of PF

The official data in the real estate market states that the supply of commercial land is decreasing, but the on-site temperature feels different. If past commercial supply was limited to planned 'central commercial areas', recently, we have seen an explosion of supply occurring in irregular manners that do not show up in the data, such as lower levels of knowledge industry centers, mixed-use developments (C-Block), and cafe streets in relocation areas.

This oversupply is rooted in the uniquely Korean PF (Project Financing) structure. Developers and construction companies must create cash flow throughout the construction period to offset low equity risks, which leads them to adopt the method of pre-selling retail space. Consequently, regardless of market demand, the structural contradiction of retail spaces flooding the market according to construction progress schedules has accumulated vacancy fatigue.

Q. Why have distribution retail spaces thrived in South Korea?

The reason for the prevalence of distribution retail spaces in the South Korean retail market is a combination of the inevitability of the development structure and the unique psychology of asset ownership in Korea. It can be summarized from two main perspectives.

1. Structural Factors of the Development Process: Risk Diversification and Early Cash Flow Acquisition

Firstly, domestic real estate development generally proceeds through PF (Project Financing) based on minimal equity. From the perspective of developers and construction companies, they must settle massive construction and project costs within the 4 to 5 years of construction, making pre-selling retail spaces to recover interim payments the most efficient funding method. In other words, distribution retail spaces were utilized as a key device to diversify the development project's risks and secure cash flow.

2. The Psychology of Physical Asset Ownership: Capital Gains Overwhelming Yield

Another reason is the strong investment psychology towards physical asset ownership. South Korean investors have a very high preference for securing individual ownership rights, including land shares. Particularly in core locations like Gangnam, even though rental yields drop below 2%, which is irrational in terms of operational efficiency, the symbolic nature of owning a shop in Gangnam and expectations for land price increases have driven investment. The psychology that values capital gains over yields has also played a role in sustaining the distribution retail space market.

Q. Why, despite stable supply indicators, is the field experiencing the highest level of vacancy fatigue ever?

1. The Pitfalls of Data: The Terrifying 'Hidden Supply'

First, while the official supply indicators for commercial land maintain levels similar to the past, the market's perception of vacancy fatigue is at an all-time high. This is due to irregular supply occurring in the blind spots of statistics. Although the total amount of designated 'central commercial land' is limited, the actual market has been flooded with retail spaces within residential projects, retail below officetels, and support facilities within knowledge industry centers, particularly the recent culprits of oversupply.

2. The Combined Effect of High Interest Rates and Declining Consumer Spending: 'Arteriosclerosis' of Local Businesses

The combination of oversupply and high-interest rates, along with weakened domestic demand, has completely drained the survival capability of local businesses. As the burdens of principal and interest payments become unbearable for investors and tenants face declining sales, the fatigue accumulates, and local businesses outside the key areas of Seoul are effectively at risk of 'shutdown'.

3. Polarization of Consumer Patterns: The Disappearance of 'Convenient Businesses'

The accumulated fatigue has changed consumer behavior patterns. Now, even with an abundance of liquidity, consumers do not shop at the 'convenient businesses' located at their doorstep or directly beneath their offices. Instead, they gravitate towards certain 'destination retail' businesses that offer clear experiences and content, leading to a fixation on this trend.

4. The Disappearance of Investment Psychology: The Reality of Yield Collapse

Currently, the retail investment market has moved beyond simple contraction to a stage where the psychology itself has vanished. In a situation where yields are not justified, fears of asset value decline dominate the market, creating a significant risk of an overall liquidity crisis in real estate assets.

From Macro Analysis to Micro Planning

In an era where the pie of retail space is shrinking, the existing broad analysis approach becomes pointless. We must abandon the macro perspective that treats the entire retail environment as a single entity and focus on detailed 'micro product planning' that closely examines the functions and competitiveness of individual buildings.

Especially in local metropolitan areas where the risk of population decline has materialized, rather than hope for an overall recovery of the retail space, we need to view our buildings as independent products and devise a 'survival of the fittest' strategy. While the sector may shrink, it will not disappear, so only those buildings that secure definitive functional advantages within the reduced pie will survive.

Category

Macro Approach (Past)

Micro Planning (Present)

Target of Analysis

Overall foot traffic in the retail sector and backing households

Vertical circulation and unit competitiveness of individual buildings

Core Strategy

Filling by product type (Quantity)

Positioning based on functionality (Quality)

Solutions

Attracting tenants through rent adjustments

Re-evaluating asset value through Value-Add

Q. What indicators do you consider most important when diagnosing local retail projects?

1. Precise Diagnosis

In local retail areas, the physical competitiveness of the assets, rather than external inflows, determines success or failure. Therefore, before examining the overall flow of the retail sector, we must first analyze the micro elements of the hardware, checking if the building's circulation is not closed off, and if accessibility from the underground parking lot to the store is effective, as these aspects will help assess the asset's self-sustaining capability and potential.

2. Quality Control

Simply segmenting units to fill vacancies with low-performing industries (such as real estate, mobile phone stores, etc.) may be advantageous for short-term exits, but it destroys the building's longevity and asset value. A thorough investigation must be conducted to ensure that tenants are continuing normal operations within the boundaries of their rent resistance and that they are high-quality tenants paying reasonable rents in line with the market. This information will be foundational for renovations.

3. Feasibility Review of Strategies

Even the optimal strategy proposed by consultants is useless if it lacks the rental capacity to be implemented. A detailed check of the willingness for hardware investment for building improvements, as well as the financial capacity to manage rent adjustments or promotional costs, must be done beforehand. Prioritizing the client's needs while finding feasible 'compromises' within realistic constraints is the essence of practical planning.

4. Professional Approach for the Sustainability of Distribution Retail Spaces

In the case of local distribution retail spaces, complex issues such as adjusting interests with individual owners are prevalent. Thus, a specialized and multifaceted consulting approach that can maintain the asset’s value in the long term is essential, going beyond simple leasing.

Deriving Realistic Compromises for Sustainable MD Configuration

One of the causes undermining asset longevity is the distorted supply structure driven by maximizing sales profits. Developers may unjustifiably split retail spaces to justify high selling prices or fill MDs only with properties that can afford high rents, such as real estate or mobile phone agencies, disregarding the context of the retail environment.

This fragmentation of space and qualitative degradation of tenants ultimately causes the loss of the asset's attracting power, blocking any future efforts for consolidated management or value enhancement.

Q. What argument do you use to persuade clients in a market situation with strong rent resistance?

Tenants are knowledgeable about data and sensitive to market prices. It’s a market where tenants hold the upper hand, and flattery won’t work. Hence, while maintaining face rent, it is necessary to adopt a technical approach that utilizes promotional costs like rent-free periods or interior support (TI) to ease tenants' initial burdens.

Q. Why are anchor tenants like Starbucks or Paul Bassett important?

1. The Trickling Effect of Attraction and Establishing Coordinates in the Retail Sector

Anchor tenants serve the role of establishing what we call 'coordinates' for the building. Brands like Starbucks or Paul Bassett become powerful destinations themselves, drawing in external foot traffic. While they might require sales-based commissions or low rent, resulting in lower short-term profitability, the attracting power they create becomes a decisive catalyst for renting out the remaining small MD units.

2. Trustworthiness from the Financial Sector and Core Variables for RTI Evaluation

When calculating the key indicator for commercial real estate loans, RTI (Rent To Interest), having a high-quality entity like Starbucks within the premises increases the stability and sustainability of rental income, leading to a favorable assessment.

RTI Criterion: For non-residential (commercial) properties, meeting an RTI of 1.5 times or more is necessary to facilitate loans (based on current financial sector guidelines).

Increase in Collateral Value: Retail spaces inhabited by high-quality brands are categorized as 'creditworthy assets' by financial institutions, placing them in advantageous positions regarding loan-to-value (LTV) ratio or interest conditions.

3. Securing Saleability and Ensuring Liquidity for Exit

For developers, the mere title of 'anticipated tenant of Starbucks' becomes a powerful sales marketing tool, and for sub-buyers, it offers a guarantee for high liquidity based on stable operations without worrying about vacancies, enabling them to realize capital gains.

The Essence of Retail Does Not Change

While the crisis discourse surrounding retail is prevalent, it should be interpreted not as the end of the industry but as 'a transition in business formats'. Even if large supermarkets face crises, warehouse models like Costco or E-Mart Traders, or online-integrated models like SSG take the lead in the market. As housing regulations tighten and the desire for cash flow for retirement grows, retail spaces remain attractive investment opportunities. However, a heightened perception is now required—one that invests in proven products rather than merely making investments based on blueprints.

Q. Where are the positive signals for the future of retail investment?

Consistent income of 1 to 2 million won makes retail spaces the most attractive investment option. The inherent value of being able to generate cash flow while avoiding risks from housing regulations remains valid. However, the era of simply building and selling is over. The market will be restructured not merely by 'location' but by execution capabilities such as the following:

Redefining the Purpose of Space: It is essential to clearly define what function (Hub) the building will perform within the community, going beyond simply filling product types.

Value Management Period (Asset Management): Moving away from the mindset that 'exit' happens once a sale is made post-distribution, the ability to maintain tenant sustainability and increase asset value during operational phases will be crucial for investment success.

Data-Based Precise Targeting: The market will only survive through product planning that microscopically analyzes the lifestyle of core targets that actually open their wallets, without being bogged down by macro foot traffic figures.

Ultimately, what we need now is the ability to identify 'real products'. As seen in the case of Gwanggyo El Port, when meticulous MD management by developers harmonizes with appropriate tenant placement, asset value will finally be realized.

I believe that now, when the market has cooled down, is an opportunity to focus on fundamentals. It is not that all retail spaces are sinking into an abyss of vacancies; rather, it is the time to transform with more sophisticated functions and refined retail strategies. As players in the distribution market, we must uncover sustainable content and maintain it consistently to prove 'true value'.

More in

More in

market

market

market

Apr 2, 2026

Office Retail: No Longer the Sidekick

Beyond rental spaces, office retail determines the sophistication of an office.

market

Mar 4, 2026

The reason why choosing a flagship store location based on intuition can lead to disaster.

The 'Golden Rule' for successful location selection proven by data from 31 industry experts.

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam

Get the best of 'detail'

in your inbox, every month

Once a month, no spam